The Greek Crisis Was Planned!

Europe is at a crossroads

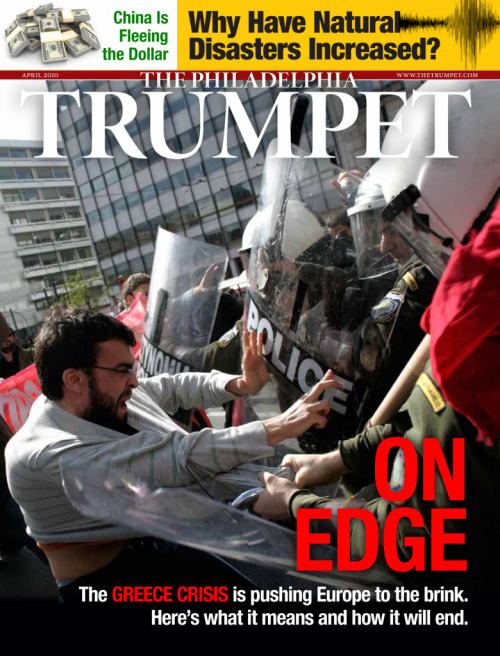

Greece is on the verge of collapse. This Mediterranean nation cannot pay its debts without massive restructuring.

Both French and German ministers have announced that they will not bail out their Club Med neighbor. Instead, EU monetary authorities are pushing Greece to massively slash its budget. But if Greece were to implement the severe spending cuts needed to get its deficit under control, it could easily plunge into an even deeper recession. Also, loss of government handouts has already created mass strikes and social unrest—a trend certain to get worse as the cuts become more steep.

Yet if Germany and France allow Greece to continue defying its monetary agreements, there will be little to stop other deeply indebted countries like Spain, Portugal and Ireland from also reneging on their monetary commitments. The credibility of the euro would be thrown into doubt.

All eyes are on Europe. Can the euro survive if Greece leaves or is kicked out of the monetary union? If a bailout comes, who will fund it, and at what cost?

There are no good choices. All of them will be very costly. Greece’s massive debt problems threaten the very viability of the European Union.

The disparate nations of Europe are desperately seeking a savior.

The truly remarkable thing is, this crisis was no accident. Not only was it eminently foreseeable long ago, but evidence suggests that it was deliberately planned. And its outcome promises to unfold just as its authors hoped.

What is happening in the European superstate is a mystery to most of the world. Yet while stock markets gyrate and bond investors panic, Trumpet readers know the ultimate result.

“The crisis in Greece is a forerunner of a whole rash of similar crises set to soon break out across Europe,” editor in chief Gerald Flurry wrote in the February 2009 Trumpet. “They will provide the catalyst for the EU’s leading nation,Germany, to rise to the fore with solutions of its own making.”

For more than a decade, the Trumpet has warned about the rotten heart of Europe. We have specifically noted the flawed currency exchange rate mechanism and how the structure of the EU was a Trojan horse for stealthy German ambitions.

“Who will get control of this great superstate?” asked Mr. Flurry in June 2000. The battle comes down to two nations—France and Germany, he said. But it will be the nation that controls the money—Germany—that will ultimately reign supreme.

Today, events unfolding in Europe are proving that forecast uncannily accurate.

Created to Fail?

From the beginning, the euro was destined—maybe even designed—to fail. At least that is the conclusion of some analysts.

Back in 1992, the power elites in Europe enticed the hapless member nations of the EU at that time into signing up to the Maastricht Treaty on European Union. The treaty contained a vital clause creating the foundation for an economic and monetary union—emu. This has become synonymous with the subsequent European Monetary Union, also called the emu.

The emu was glued together by a single currency. The euro was introduced in 1999, with notes and coins entering circulation in 2002. To date 16 EU member nations have joined the emu, sacrificing their individual national sovereign means of exchange—and in the process setting themselves on a course that would lead to the total sacrifice of their national sovereignty on the altar of the imperialist project of the European Union.

After the EU single currency system was implemented, certain voices predicted the failure of the euro. A handful theorized that the euro may well even have been deliberately created to fail by certain German elites. The theory was that Germany would bide its time and allow the unworkable monetary union to prevail till it reached a point of collapse and then, having wrested control of the European Central Bank (ecb) out of any competitor’s hands (read France, in particular), move in quickly and take direct control of emu administration. Germany could then ensure that a preferred core of EU member nations would receive ecb favor, with the disfavored reduced to vassal status or worse.

Why, if the theory is correct, would Germany deliberately create an economic and monetary union that was destined, from all the tests applied by the clearest thinking observers at the time, to fail?

Unification Through Stealth

When the eurozone’s founders began working toward pan-European unity, they knew it would be virtually impossible to unite the Continent. Jean Monnet, one of the forefathers of the European Union, was well aware of the difficulty of convincing voters to willingly relinquish their national sovereignty. Monnet felt that the only way to achieve unification, without war, was through stealth. The people must not know that sovereignty has been surrendered until it is gone.

English conservative and author Adrian Hilton described Monnet’s intentions for Europe this way: “Europe’s nations should be guided towards a superstate without their people understanding what is happening. This can be accomplished by successive steps each disguised as having an economic purpose, but which will eventually and irreversibly lead to federation” (The Principality and Power of Europe; emphasis ours throughout).

As Monnet said on April 30, 1952, “The fusion [of economic functions] would compel nations to fuse their sovereignty into that of a single European state.”

Peter Thorneycroft, former chancellor of the Exchequer of the United Kingdom and Europhile, described the Monnet unification method in a 1957 Foreign Affairs article: “The idea of a united Europe is not new. It has exercised the minds of the soldiers and sometimes of the statesmen of Europe for many centuries. … Torn by war and conquest, weakened by internecine strife, Europeans have yet found the time and the capacity to leave an incomparable legacy ….

“Yet men do not live easily within the same institutional arrangements. National patriotisms are strong ….”

In an earlier booklet, Design for Europe (1947), Thorneycroft wrote: “No government dependent upon a democratic vote could possibly agree in advance to the sacrifice which any adequate plan must involve. The people must be led slowly and unconsciously into the abandonment of their traditional economic defenses, not asked, in advance ….”

Economic integration, once initiated, would become self-sustaining, it was hoped. Monnet theorized that economic interdependence would drive integration until eventually, Europe would end up with de facto political centralization and unification.

Today, Europe may be at a tipping point where economic integration finally meets political unification.

“The European experiment with a trans-sovereign currency is facing its first acid test,” wrote Euro Pacific Capital’s John Browne. “In essence, the euro was created as a lever to encourage a complete European political union rather than as a currency representing … an already unified economy” (February 10).

According to Browne, who is a former British member of Parliament and close associate of then Prime Minister Margaret Thatcher, the euro has largely succeeded in creating the will for a federal Europe among the political classes even though European citizens have voted again and again to maintain their individual country’s sovereignty.

“Whoever controls the currency controls the government,” said economics guru Maynard Keynes. To him, that was not just a law of economics; it was a law that underwrote power politics.

Anticipated Crisis

When the euro was created, a chain of events was set in motion. For nations like Greece, a future debt crisis was almost inevitable.

By joining the eurozone, Greece traded its inflation-prone drachma for the stability of the euro. It also gained the economic borrowing clout of a superstar, even though it had the economy of a small supporting actor.

Initially, these two advantages vastly improved the standard of living for the people of Greece. They allowed corporations, individuals and government to borrow money at the low rates typical within large developed countries like Germany. The new low interest rates were more than Greece could resist. All levels of society binged on seemingly cheap money. The government, for its part, embraced a massive welfare state, also made possible by easily obtained low-interest loans.

But as lenders to Greece are beginning to remember, there was a good reason Greece paid far higher interest rates to borrow money when it was not a member of the Union. Greece has a history of borrowing too much. According to analyst John Mauldin, Greece has been in default in one way or another for 105 out of the past 200 years.

Even as luxury swiftly came to Greece, so now have the first whiffs of poverty.

With a projected budget deficit of 12.7 percent of the nation’s gross domestic product, Greece is far out of compliance with the eurozone’s mandated 3 percent maximum. With the world in recession, investors are wondering how Greece will pay its bills.

Typically when a country takes on too much debt, it contracts Argentine-disease. Known also as “quantitative easing,” countries devalue their currency by turning on the money printing presses and simply creating the currency to pay the bills. This of course upsets creditors, but at least the bills get paid. The economy also gets a short-term kick-start because a devalued currency makes exported goods less expensive; thus foreigners buy more domestic products.

Greece, however, does not have this option. Since it is locked into the euro, it does not control the printing presses. Germany does.

Analysts worry that Greece may be reaching the point where a debt spiral could bankrupt the government. What will Europe do?

It’s true that the Greece crisis will necessitate some difficult and costly decisions. But in some respects, as far as the European political class is concerned, it matters not whether Greece stays or goes. Greece is a peripheral country, immaterial to the desire for a federalist Europe. What is material is that the current crisis be exploited to its maximum—and that means that it be used to foster further integration of core Europe.

Will the Eurozone Be Pared Down?

The Telegraph’s Ambrose Evans-Pritchard wrote on January 31 that the solution to the crisis could involve a paring down of the eurozone. He noted the possibility of a bloc of nations centered on Germany leaving the eurozone and creating a new currency: the Deutsch mark 2. The rest of the eurozone countries would then be free to devalue the euro (turn on the printing presses) to pay down debts.

Although Evans-Pritchard noted that Germany is currently happy with its advantageous position within the euro, he also said there would be certain benefits to a newly created German-led bloc.

Events in Greece bear close watching, especially in light of the advent of the seventh revival of the Holy Roman Empire in Europe, which officially began on January 1 with the onset of the Lisbon Treaty.

The first major reason to watch this issue is that the Bible indicates that this final Roman imperial resurrection will be composed of 10 nations or groups of nations (as indicated in Daniel 2). Whether or not the current 27 EU nations get regrouped into new political regions remains to be seen, but the economic crisis in Greece may well provoke a vast restructuring or paring down of the European Union.

Far from heralding the end of the European unification project, the current crisis in Greece may actually signal a new beginning.

Forcing the Pace of Political Union

Back when the euro was first created, the European Commission’s top economists warned politicians that the new currency might not survive a serious crisis. They knew that because the eurozone had “no EU treasury or debt union to back it up” and a “one-size-fits-all regime of interest rates [that] caters badly to the different needs of Club Med and the German bloc,” the day would come that economic crisis would threaten the EU (Telegraph, Oct. 1, 2008).

The fathers of the euro did not dispute this. They knew European economic union was risky, but they saw it as an acceptable risk—even desirable—as a last-ditch option to force the pace of political union. As the Telegraph said, “They welcomed the idea of a ‘beneficial crisis.’” And as “ex-Commission chief Romano Prodi remarked, it would allow Brussels to break taboos and accelerate the move to a full-fledged EU economic government” (ibid.).

Mr. Flurry’s words from that February 2009 article ring out: “Berlin has been planning for this crisis before it even adopted the euro. European elites knew it would eventually come. And they will soon present a solution.”

Sure enough, in the midst of the Greek crisis, an increasing ensemble is crying for a federalized European economic government—one with not just a common currency, but one with a common debt union and power structure—kind of like a United States of America in Europe.

It is “Time for the Eurozone to Grow Up,” headlined the Wall Street Journal on February 8. There is a way out of this dilemma, it wrote. “It would require a European federal government with substantial taxing and spending power, with the ability to redistribute resources and impose fiscal discipline across the continent. In short, it would require a far greater degree of political union …. Yet the choice is now clear and inescapable.”

That is exactly the kind of talk that political elites are looking for. It is also a sentiment echoed in Europe.

“The crisis has revealed our weaknesses,” said European Union President Herman Van Rompuy in February. “Recent developments in the euro area highlight the urgent need to strengthen our economic governance.” Europe needs a powerful “economic government,” he said.

The EU’s foreign affairs chief, Catherine Ashton, agrees. More political union is needed, she said on February 6 at the Munich Security Conference. “We must mobilize all our levers of influence—political, economic, plus civil and military crisis management tools—in support of a single political strategy.”

“The days when a common EU foreign policy was regarded as mere talk are numbered,” Ashton said.

Yes, the days when the free nations of Europe charted their own destiny are indeed numbered.

Victory for Berlin

Consider the success of the euro project in the grand scheme of things. By gearing a whole continental economy to a single currency—imposing rules for membership of monetary union that it was clear no member nation could reliably and consistently fulfill—the German elites crafted a scheme designed to create a continental crisis. If they come to control the ecb (and judging by the top candidates for the presidency, which is due to change hands next year, this looks to be a done deal), they will be positioned to respond to that crisis by enacting, at their will, a totally reconstituted European monetary union.

Such a union will vest financial and economic power in the hands of a select group of nations. These core nations will act in consortium under Berlin and Rome’s direction to propel the Holy Roman imperial vision to reality. They will no longer be frustrated by having to seek a majority vote from 28 fractious, disparate EU member nations. The weaker nations will simply become slaves to the beck and call of the ecb, beholden to it and its governing authority for their economic survival—a literal fulfillment of the prophecies of Revelation 13.

Whether or not the euro fails under its present stress doesn’t change this reality: Given the likely imminent placing of a German in charge of the ecb, Germany is about to directly control the bullion hoard stashed in the vaults of the ecb and beyond. The ecb is headquartered in Frankfurt; the importance of the German elites ensuring the bank lies in Germany’s heartland will prove a vital key in securing the bank’s wealth in times of crisis. When financial crisis arises, Germany will control the EU’s singular currency and hence imperial power over the whole of the EU. It will be a case of game, set and match to Germany.

Some have even mused that, as the day of monetary crisis approaches, the German elites, having positioned themselves to seize control of the ecb, would use an appropriate global institution under EU dominance as a regulator to both control and regulate global trade in the EU’s favor.

As regular Trumpet readers know, the Bible indicates that a king will soon arise in Europe who will deceitfully gain power and force his authority on Europe. The machinations for this pan-European federalist hijacking are falling into place.

Dictating Europe’s Destiny

The second reason the Greek crisis bears close watch is that the Bible indicates that this European superpower will be dominated by Germany. If this crisis in Europe has shown anything, it is that, at least economically, Germany holds ultimate power in Europe.

Bailout or no bailout: Either way, Germany wins. If Germany and Europe bail out Greece, what will be the cost? If Germany has to ask its citizens to reduce their standard of living to subsidize Greeks, what will it ask Greece for in return? The price is sure to be steep. Conversely, if Germany were to work to remove Greece from the EU, the result would be a slimmer, economically healthier, core Europe with one less voice to dilute German political clout.

Sixty-five years after World War ii, Germany is again dictating the destiny of Europe. This should startle the world.

As Britain’s Iron Lady, Margaret Thatcher, warned in 1993, “You have not anchored Germany to Europe. You have anchored Europe to a newly dominant, unified Germany. In the end, my friends, you’ll find it will not work.” It is Germany’s national character to dominate, she said.

Germany has hijacked Europe. Greece knows it. Portugal and Ireland will find out next. And probably Britain soon thereafter.

But remember: You read it here first.

Prophecy Fulfilled!

The true portent of all that is happening in Europe will only be obvious to those who understand the reality of the prophetic words of that once “ambassador for world peace without portfolio,” Herbert W. Armstrong.

Relying on the Bible for his vision of the future—and on a deep understanding of world events, coupled with his high-profile discourse with the upper echelons of international leadership—Herbert Armstrong powerfully proclaimed these events that have occurred in Europe, especially since the unification of Germany, itself one of his most oft-repeated prophecies. Fully five years before World War ii, Herbert Armstrong prophesied these events. He continued to air those same prophecies while Germany lay in abject defeat, then on throughout the wirtschaftswunder—the German economic miracle of postwar revival—clear on up to his death four years before the fall of the Berlin Wall and the resultant reunification of Germany.

Ten years before the wall fell—13 years prior to the signing of the Maastricht Treaty which created the European Monetary Union—Herbert Armstrong declared, “I have been proclaiming and writing, ever since 1935, that the final one of the seven eras of the Holy Roman Empire is coming in our generation—a ‘United States of Europe,’ combining 10 nations or groups of nations in Europe—with a union of church and state!

“The nations of Europe have been striving to become reunited. They desire a common currency, a single combined military force, a single united GOVERNMENT. They have made a start in the Common Market. They are now working toward a common currency. Yet, on a purely political basis, they have been totally unable to unite. …

“This new united Europe will be, militarily and economically, as strong, or even more powerful, than either the United States or the ussr. It will be a third gigantic world power! But it will be exceedingly short-lived (Revelation 17:10, 12)—as iron and miry clay are not adhesive, and will not stick together (Daniel 2:42-43)” (Plain Truth, January 1979).

In our February edition, our editor in chief proclaimed that, as of Jan. 1, 2010, “The Holy Roman Empire Is Back!” That ought to be a call to action to those who once heard and believed Mr. Armstrong’s words. If those words ring in your ears today, then you ought to realize the time for delay in your returning to the only way of life that guarantees true freedom, safety and protection from this seventh and final resurrection of the Holy Roman Empire is up! The words we publish are a powerful warning to you in particular!

The ball is in your court. The door is before you. Christ said all you have to do is knock, and He will open unto you!