What Does Free Money Cost?

If you don’t save for the future, you will starve. This is a truth that people learned from early in human history. It is obvious to all who farm, hunt and preserve food, and who watch the weather and climate. It is an ancient principle put into practice long before the creation of money, credit and just-in-time inventory management. Saving for the future is what people everywhere used to believe in.

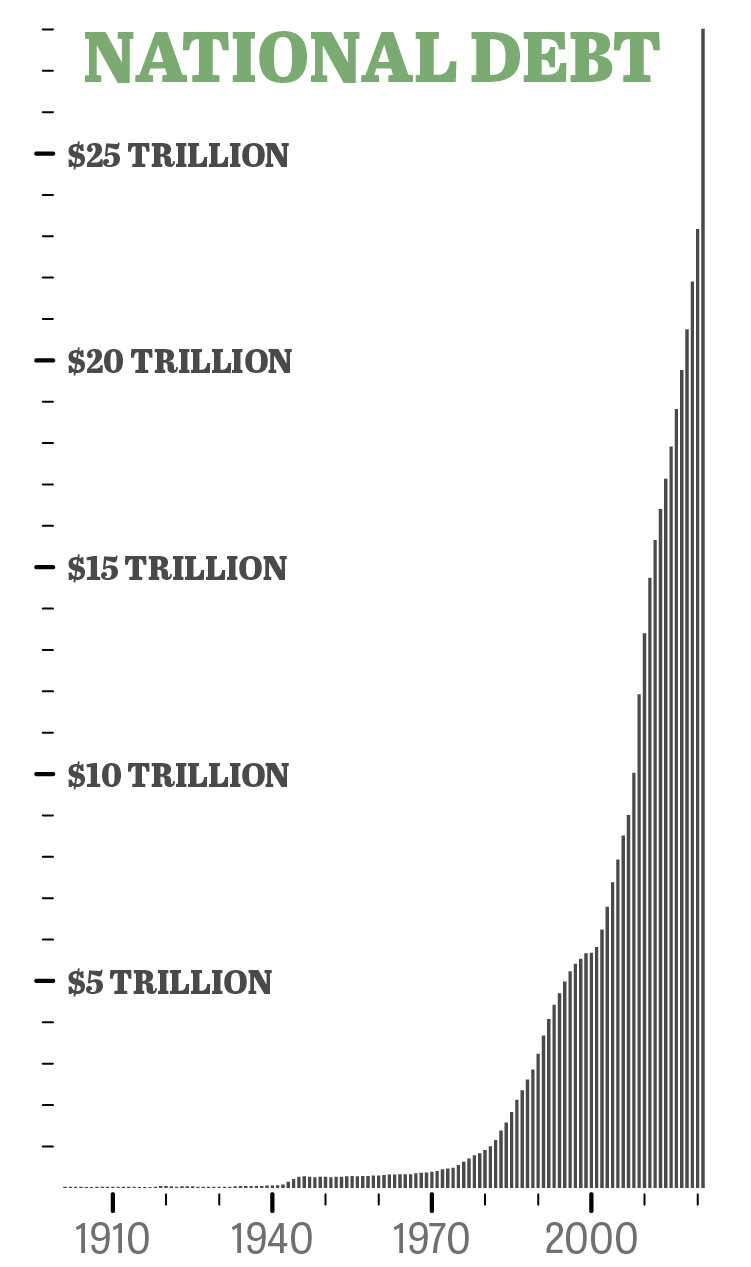

Today, the United States is $28 trillion in debt. We have no savings. There is no emergency fund. We have already spent the taxes on future earnings of our grandchildren—and their children.

But if you believe America’s leaders, everything will be fine because none of that matters anymore.

Leaders in Washington, Wall Street and even Main Street believe in a new economic theory. Politicians love it, because it makes saving for the future obsolete. It theorizes that deficits and debts are actually good because their main effect is to stimulate the economy. It theorizes that we won’t ever really have to pay back borrowed money because our central bank can create unlimited numbers of dollars out of nothing—at the push of a button. The theory has a name: Modern Monetary Theory. Believers view it as a modern monetary miracle, a way to push economic problems into the future forever.

These theorists think they have transcended the basic laws of economics.

Can you borrow money and spend it without ever having to pay it back? Can you print massive amounts of money out of thin air without destroying its value and making everything more expensive?

We are going to find out.

Print and Spend

Since the onset of the covid-19 lockdown and resulting economic fallout, the Federal Reserve has increased the nation’s money supply to record levels. Over the past 12 months, the M2 money supply—which includes cash, checking accounts and other easily spent money—has ballooned by more than 27 percent!

In other words, one out of every five dollars of all the easily spendable money in existence since the founding of this nation was created over the past 12 months. And the Federal Reserve has used much of that money to buy trillions of dollars of government bonds, treasuries and even people’s mortgages.

This is how it works: The U.S. Treasury prints a bond, which is basically just a promise to pay back borrowed money with interest. It sells it to the Federal Reserve in exchange for dollars that the U.S. government then spends. Where does the Federal Reserve get dollars to buy bonds? This is where the modern monetary miracle comes in. The Fed doesn’t earn dollars by providing goods or services or anything else, or even by collecting taxes. It creates dollars out of thin air. It has the ability to add as many zeros to its bank account as Washington wants. With the push of a keyboard button, it can expand its dollar supply to approach infinity.

But according to the Federal Reserve, there is nothing of concern here. In March, it quietly announced that it will no longer publish weekly data showing the number of dollars coming into existence.

“They are trying to hide something,” said Steve Hanke, professor of applied economics of Johns Hopkins University. “They don’t want people paying attention to money supply growth.” As Hanke pointed out, “[Federal Reserve] Chairman [Jerome] Powell has very explicitly claimed that money doesn’t matter in recent testimony. He’s basically said that money and the measurement of money doesn’t really matter because it’s unrelated to inflation.”

Hopefully Mr. Powell is right, because the U.S. government is spending a lot of it. Consider the scope of the “stimulus” bills over just the past 12 months:

$2.2 trillion for the Coronavirus Aid, Relief and Economic Security Act of 2020.

$2.3 trillion for the Consolidated Appropriations Act of 2021.

$1.9 trillion for the American Rescue Plan Act of 2021

$6.4 trillion! Where did all that money come from?

Some of it was borrowed and will have to be paid back with interest. But an incredible $3.6 trillion worth was created with the stroke of a pen and a push of a button.

Pantera Capital gives some context. With the first trillion dollars the United States printed throughout its history, “We defeated British imperialists, bought Alaska and the Louisiana Purchase, defeated fascism, ended the Great Depression, built the Interstate Highway System, and went to the moon.”

What did we accomplish this past year with $6.4 trillion?

Initially, the government distributed money to businesses and individuals, many of whom had lost income because the government shut down much of the economy. This was one of the first times in American history that the government gave direct cash handouts to individuals. The government also increased unemployment benefits and issued grants to businesses. But much of the money went to other uses.

Now more than a year has passed since the first covid lockdowns. Official unemployment has dropped back down to just over 6 percent, gasoline demand is approaching pre-covid levels. Housing prices are setting records all over the nation. And the stock market is reaching record highs.

Yet the stimulus spending plans are not even close to over.

Looming Inflation

The Biden administration is currently working on a $2.3 trillion infrastructure bill in addition to another $2 trillion American Families Plan infrastructure bill. “Together, the ideas inside these plans aim to redefine what infrastructure is, by bolstering ‘human infrastructure’ along with everything else,” writes Slate. “[It’s]a new kind of American populism.” More accurately, it’s American socialism.

This spending comes in addition to the regular $1 trillion budget deficits the government was running before it began shutting down the economy.

And contrary to Fed Chairman Powell’s claims, the economic laws of supply and demand are asserting themselves. More money (due to money printing, government spending and government handouts) chasing a constant or shrinking supply of goods (due to the global lockdown) means the same goods and services cost more dollars.

“A little inflation feels good at first, because wages are rising, and people feel richer,” investment adviser Jared Dillian said. “But the laws of economics are not to be conned. What Powell is doing is what I call central bank populism. [T]here is inflation in the beginning. At the end, there is revolution.”

Notice the price of lumber lately? A sheet of plywood at your local hardware store now costs more than $65. A standard 2×4 costs $7. Average lumber prices have surged close to 200 percent over the past year. Why? Because of supply shortages due to government-mandated factory lockdowns and soaring demand due to people with government handouts remodeling their homes.

Gasoline is also becoming more expensive, with prices nationwide averaging $2.86 per gallon before the summer driving season has even hit. Corn is up 67 percent year over year. Corn syrup is in just about everything. Wheat is up 24 percent. Milk is up 9 percent.

This is not just happening in America. Governments worldwide are printing money to spend. Prices for basic necessities like food are rising. The United Nations Food and Agriculture Organization reports that food prices are up 24 percent over the past year to the highest levels since 2013. Remember the Arab Spring? Some say that, like so many revolutions before it, it began as a hunger revolt.

Other commodities are costing more dollars this year too. Copper: 82 percent more. Silver: 62 percent more. Texas oil: 28 percent more. Concrete: 60 percent more.

Powell and the Fed assure us that the inflationary effects will be moderate and temporary. His comments sound eerily similar to former Fed Chair Ben Bernanke’s comments that the subprime mortgage bubble was contained. That infamously led to the Great Recession of 2008.

One big difference between that crisis and this one is where the Federal Reserve has directed its response. In 2008, the money it created through quantitative easing was injected into the banking system. It caused asset inflation in financial sectors like the stock market and the housing market, but it kept the banks from collapsing and caused less inflation in consumer goods than many people feared. This time, the cash is being sent directly to individuals and businesses. When spending increases, the velocity of money could send inflation soaring and the value of the dollar plummeting.

In other words, massive money printing did not fix the fundamental economic problem in 2008, nor has it fixed the problem this year. We temporarily papered over a volcanic economic upheaval, and it cost us mountains of money to do it.

“Two years, we will be at $40 trillion in debt, and in two years after that, if we continue this stimulus we are going to be at $50 trillion” said Jim Puplava at Financial Sense Wealth Management. “At some [point], these debt levels are unsustainable.”

The U.S. government was running trillion-dollar deficits under presidents Barack Obama and Donald Trump. And that was in relatively good times.

“If you are spending $6 to $7 trillion per year to stimulate the economy now, when the economy is recovering, what do you do when you get into a recession?” Puplava said. “How big will the stimulus have to be to get out of the next recession or depression?”

How sad that we are even asking this question. America is the wealthiest nation in world history. Yet its economy is doomed.

Why doesn’t America manage its resources better?

An Ancient Lesson

Before taking office, all politicians should read Genesis 41. So should Federal Reserve chairmen and secretaries of the Treasury. Our worsening boom-bust cycles, our imminent social upheaval, the causes of so much suffering would be avoidable—if we had the humility to learn.

God inspired the leader of the wealthiest and most powerful nation in the world to have a dream. One of its vivid, haunting scenes was seven fat, healthy cows being eaten by seven emaciated, sick cows. He could not get the dream out of his mind, and none of his advisory staff at the capital could tell him what it meant or what to do.

Then one of his staff remembered a certain imprisoned slave. He was brought in, and said that the dream meant the nation would enjoy seven years of fantastic abundance, followed by seven years of famine. He advised that the leadership save during the good years so that the nation could survive the lean years.

This is the record of how God used Joseph to advise the pharaoh of Egypt. You might know the story. So too might many of our modern politicians, economic wise men and financial magicians. But they reject the lesson: You must save for the lean years!

Even during the best years of the last two presidential administrations, not once did the government run a budget surplus. It took in record amounts of revenue through taxes, yet spent even more. The national debt took more than 200 years to reach $1 trillion. It took only 26 more years to rise to $10 trillion in 2008, and only 12 years to exceed $27 trillion. Our national debt is now greater than the sum of all goods and services all Americans produce in an entire year. Yet our leaders—and many of us—refuse to change our behavior and comply with economic laws of cause and effect.

At least during President Trump’s term, he cut taxes, allowing people to save more of their income. But which of us did? Did a single politician even worry about the rising debt during the last presidency?

America’s leaders have instead motivated people to eat their grain, then borrow grain from their neighbors (and other nations) and eat that too!

When the government shut down the economy citing covid-19, no one was prepared. The store houses were empty. America had to resort to even more radical, even more dangerous monetary extremes to keep the economy going.

Heeding Joseph’s advice would have prevented much of this mess. Had Americans saved instead of spent, denied themselves instead of indulging themselves, they and their government would have abundant savings to fall back on to survive the lean years—and we would not be implementing make-believe monetary policy that is guaranteed to inflict future lean years on ourselves.

Instead, America has an increasingly sickly currency and an enormous pyramid of debt.

Pharaoh was smart enough to heed Joseph’s advice. When the famine struck, the people of Egypt had food to eat, probably preventing a revolution. The economies of neighboring nations were destroyed, and Egypt actually grew even wealthier as both Egyptians and foreigners were forced to sell their flocks and herds and other wealth to the Egyptian government in exchange for food.

If America had obeyed the fundamental laws of economics rather than becoming an even more greatly enslaved debtor nation, it could have become a creditor to the world. As Proverbs 22:7 says, “The rich ruleth over the poor, and the borrower is servant to the lender.”

Heed the Lesson!

By following Joseph’s advice, Egypt went into the crisis from a position of strength and turned into a superpower. Pharaoh promoted Joseph to second in command. He was given such high esteem that his family was granted the choicest agricultural land in Egypt, and when his elderly father later died, the Egyptians mourned him as if he were one of their own.

The good news is that, even if America refuses to learn this lesson, you can. God wants you to prosper, even during severe economic depressions. Joseph’s name became synonymous with prosperity. “And the Lord was with Joseph, and he was a prosperous man …. And … the Lord made all that he did to prosper in his hand” (Genesis 39:2-3). Those who obey God’s laws do face trials and tests—Joseph is a prime example. But if God could take an unjustly enslaved, unjustly imprisoned foreigner and prosper him in character, stature and wealth, He can prosper you, no matter your condition.

God prospered Joseph for a reason: Joseph understood and followed God’s laws.

Believe it or not, this whole world could soon have the opportunity to benefit from Joseph’s economic management.

Longtime readers of this publication know that the economic situation for America and the nations of the world is hopeless. Yet God will soon personally intervene and save humanity from itself, from lawless thinking that plunges us into disaster, suffering and death (economic and otherwise). When Jesus Christ returns, as the Bible prophesies, He will return to assume governance of all nations. He will teach and enforce God’s law. He will inspire and compel human beings to follow the laws of cause and effect that produce peace, prosperity and purpose (see Micah 4:1-4).

In his booklet The Wonderful World Tomorrow—What It Will Be Like, Herbert W. Armstrong described this future time, when people will obey God’s laws of economics worldwide: “[Joseph’s] specialty was dealing with the economy—with prosperity. And what he did, he did God’s way. It seems evident, therefore, that Joseph will be made director of the world’s economy—its agriculture, its industry, its technology, and its commerce—as well as its money and monetary system. …

“Undoubtedly Joseph will develop a large and perfectly efficient organization of immortals made perfect, with and under him in this vast administration. This will be an administration that will eliminate famine, starvation, poverty. There will be no poverty-stricken slums. There will be universal prosperity!”

Universal prosperity! Universal hard work, saving, self-discipline, wise spending, and growth of wealth and character.

Lean years are coming. We will learn the hard way that the theories, systems and institutions of human beings are flawed to their foundations. But the Bible gives us hope for the years that follow, when human beings will finally submit to their Creator. This is our last and best and only hope, for America and for the world.