Can You Trust the Economists?

On August 24, many Americans woke up to the smell of coffee brewing and news that China’s stock market was once again in free fall. Yawn.

By 9:30 edt, a totally different aroma was infiltrating boardrooms and offices inside America’s biggest banks and Wall Street houses.

It was fear.

Suddenly, memories of the 2008 economic crash were being replayed in high-definition Technicolor with investment managers clinging white-knuckled to their computer keyboards and iPads—watching in disbelief as stock prices went into free fall. In less than 10 seconds on Monday, over 1,000 points were wiped off the Dow Jones Industrial Average. Hundreds of billions of dollars simply ceased to exist.

Analysts wondered what would happen next. Never before have the markets been exposed to such massive leverage. U.S. corporations have borrowed a stunning $9.3 trillion since the beginning of 2009. Rarely have investors borrowed such massive sums on margin.

In China too, debt is at unprecedented levels. As market analyst Doug Noland highlighted, four of the five biggest banks in the world are now Chinese owned—and their loan books have grown an astounding 80 percent over the past four years. “A bursting Chinese Super Bubble is a systemic issue—for the global economy, for global markets and for global finance,” wrote Noland (Credit Bubble Bulletin, August 17).

“As an analyst of credit and (serial) bubbles going back 25 years, there’s a recurring theme that is especially pertinent these days. … It’s always worse than you think” (ibid, August 20).

Could this be the beginning of another Black Monday? Another 1929?

For a brief period, anxiety shot so high it blew out the Chicago Board Options Exchange volatility index—often referred to as the fear gauge. The computer algorithms couldn’t handle the unprecedented volume as the index tripled. For 30 minutes, investors were greeted with patchy data and empty screens.

The last time the index reacted so sharply, bad things followed. Think 2008 Great Recession and Wall Street meltdown.

But market participants should not have been flying blind. The fear gauge was pinging all month. By the end of August, it had jumped by 135 percent—the biggest single-month gain in its history.

A lot of other signs of trouble were already evident too.

The riskier portion of the junk bond market, which many corporations are forced to rely upon for their financing needs, got absolutely massacred just days prior to the stock market mayhem. The average cost to borrow for a ccc-rated company spiked from 13 to 16 percent on August 13. It was around 7.9 percent a little over a year ago. These kinds of “vertigo-inducing” events are rare in normal times, says analyst Wolf Richter. “And there haven’t been any [‘normal times’] since the [last] financial crisis” (Wolf Street, August 15).

In July, the Empire Manufacturing Index—the all-important measure of business activity in New York State—also plummeted to levels only before seen in the last two economic recessions.

Shipping rates have collapsed, highlighting the sharp slowdown in global trade. “There is now a full-blown August storm sweeping through global markets,” writes the Telegraph’s Ambrose Evans-Pritchard (August 17).

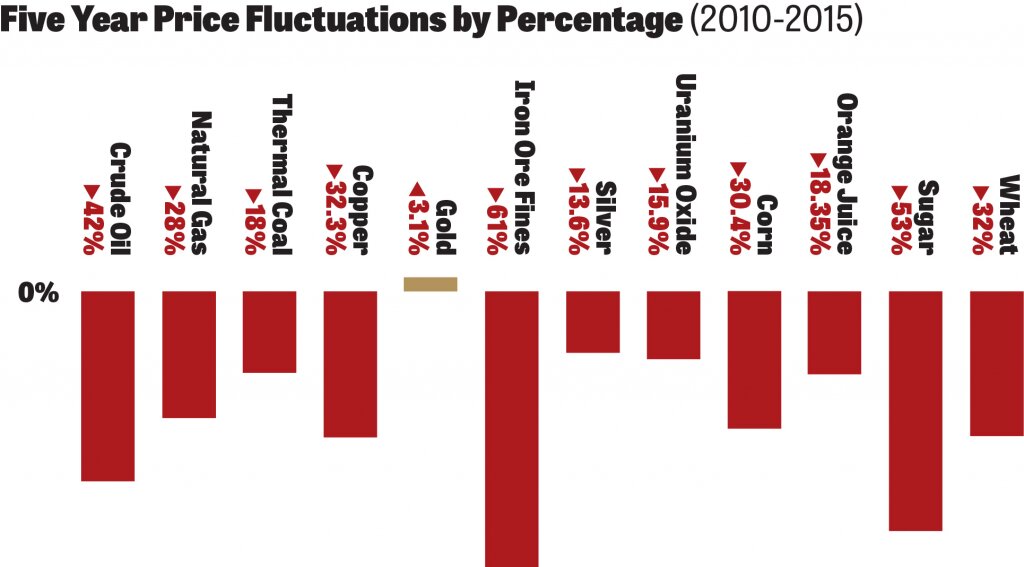

Commodity prices are collapsing too. Oil dipped below $40 per barrel on August 24, down 60 percent from a year ago. Coal, iron ore, potash, uranium, soybeans, sugar—all down. Oranges, wheat, nickel, silver, cement—all down too.

Surely somebody should have noticed that something was wrong.

On August 21, as world stock markets followed China and the United States into the red, it became clear that it had caught authorities off guard. In Australia, both Finance Minister Joe Hockey and Prime Minister Tony Abbott took to the airwaves to reassure investors after Australia’s benchmark stock index dove at the sharpest rate since 2009.

“I’m absolutely confident, absolutely confident that the fundamentals of the Australian economy and the global economy are still good, are still good. That’s, without doubt, that is the situation,” Hockey told the Nine network’s Today Show. “In fact there is no crisis now. It is a correction” (August 25).

Could he have mentioned absolutely confident one more time?

“I think it’s important that people don’t hyperventilate,” Prime Minister Abbott said. “The fundamentals are sound.” Former Federal Reserve Chief Ben Bernanke talked a lot about America’s fundamentally sound economy before the 2008 crash too.

When a prime minister is in front of the cameras talking up the market, you know that everything is not sound.

By end-of-day Monday, the Dow Jones tried to rally, but it still ended down almost 600 points. It was the first time in history the Dow had fallen by more than 500 points on two consecutive days.

The next day, the markets initially rose but the Dow ended the day down another 205 points. It was the biggest reversal since 2008.

Yet the following week saw the two biggest back-t0-back day rallies since 2009.

The markets are sending out some strong warning signs that all is not well. It is beginning to look a lot like the days prior to the last economic meltdown.

“Most crashes tend to be in the fall,” Commentary’s John Steele Gordon once observed of the crash of October 1929. “I think it’s human psychology, you tend to be more cautious in the fall. The speculations of summer that seem so brilliant, suddenly, when the chill winds of October come, you wonder if they’re such a good idea and you try to get out.” Whatever the reason—the September/October time frame does tend to be the most dangerous.

The fear gauge is at levels usually only seen in recessions. So far it has continued to rise in September. It is a strong sign that something is rotten in the state of the economy.